November 2005

Oscar Ugarteche

Institute of Economic Research

National University of Mexico, UNAM

THE RISE AND FALL OF THE IMF

The issue is whether International Financial Institutions can be

reformed or not. This paper will review the considerations in the creation

of the IMF and the riole played by the US a the time, the manner in which

the IMF has operated, the results to date and then briefly will look at

the World Bank. It begins by reviewing the debt crisis and what led up

to it in the 1970’s. There are many arguments on the roots and this paper

takes a position on a monetarist argument. Then it reviews the process

of debt rescheduling as the role of the Fund then with the adverse consequences

on the economy of Latin American countries. Then it proceeds to look at

the results of structural reforms to conclude that the institutions do

not seem to work to their own ends. It makes a review of the IMF role

in the Asian and Argentina crisis and passes review on the external debt

renegotiation mechanism and proposes in the concluding remarks another

international financial architecture without the existing IMF and with

a much reduced WB dedicated to data gathering. The paper seconds Bello’s

idea of a regional monetary fund, proposes an international board of arbitration

for sovereign debt and downplays the role of the World bank, taking from

Broad’s idea.

The creation of

the IMF in 1944 resulted directly from the instability of the world economy

during the 1930’s as a consequence of deflation that derived from the

gold standard and depression that came from the application of the beggar

thy neighbour policies plus a crisis of overproduction. The end of the

gold standard in 1933 paved the way for a new international reserve standard,

grounded on gold. This was to become the gold/dollar standard established

in 1944 at a fixed rate of US$35.70 per ounce of gold, the price at which

gold had been in the markets since the 1930’s. The reason for having the

US dollar convertible to gold was because the United States had the strongest

economy, was the world’s creditor, had the largest amount of international

reserves and the US dollar effectively served as the world monetary reserve

asset. The United Kingdom, previously a major international reserve economy,

was no longer in a position to serve that function. It had turned into

a debtor country during World War I and not withstanding that the United

States waived those debts, it again became an important international

debtor during World War II. The creation of

the IMF in 1944 resulted directly from the instability of the world economy

during the 1930’s as a consequence of deflation that derived from the

gold standard and depression that came from the application of the beggar

thy neighbour policies plus a crisis of overproduction. The end of the

gold standard in 1933 paved the way for a new international reserve standard,

grounded on gold. This was to become the gold/dollar standard established

in 1944 at a fixed rate of US$35.70 per ounce of gold, the price at which

gold had been in the markets since the 1930’s. The reason for having the

US dollar convertible to gold was because the United States had the strongest

economy, was the world’s creditor, had the largest amount of international

reserves and the US dollar effectively served as the world monetary reserve

asset. The United Kingdom, previously a major international reserve economy,

was no longer in a position to serve that function. It had turned into

a debtor country during World War I and not withstanding that the United

States waived those debts, it again became an important international

debtor during World War II.

The concept of

a currency stabilization board started developing since the 1930’s with

various currency stabilization plans being designed between 1931 and 1935.

(Eichengreen, 1989) Only when the US Treasury decided to put its pressure

to obtain it, did it work. It was when Cordell Hull at the State Department

decided that multilateralism was essential for the future of humanity

and for the stability of world peace that the concept was more properly

developed under the guidance of Harry White, pupil of Jacob Viner (1943).

The establishment of the IMF in Washington DC in 1946 was to mark not

only the importance of the institution for American foreign policy but

its influence over it. With the definite disappearance of the concept

of a board of international debt launched at the League of Nations during

the 1930’s, the issue of US Confederate State unpaid debts of the 1840’s

(CFB, 1955) disappeared from the international agenda and the new institution

was able to operate fresh on the basis of US law. It was the law of the

major creditor and major reserve holder in the world then, and is the

law for most international financial transactions after World War II.

The debt problem: a monetarist view

Most analysts place

the roots for the debt problems in major irresponsible borrowings, a large

State sector, market distortions, corruption and public sector and balance

of payments deficits. These analysts usually add to this the petrodollar

crises which raised external deficit leading to what became known as the

“debt crisis”. There are exceptions to this view such as Edwards and Larrain

(1989), Griffiths Jones (1988) and more recently Hammes and Wills (2003).

We wish to return to the U.S. interest rate analysis and the external

shock element of the crisis, in order to follow the role of the IMF in

it. James (1996: 355)) suggests that the IMF was worried in 1982 about

the impact of US interest rates and that the impact of interest rate shocks

went beyond immediate service costs

The 1970’s started

with the delinking of the US dollar from gold at a fixed rate and the

opening of the international gold and currency markets, on August 15,

1971 with the Smithsonian Agreement. It was done without consulting the

IMF and marked the end of fixed exchange rates, the scheme designed to

keep a stable world after WWII that gave the IMF its sense of mission.

The managing Director of the IMF, Schweitzer, was invited, with one

hour’s notice, to attend a meeting in the U.S. Treasury with ? Fed President?

Paul Volcker (Secretary?of the Treasury?Connolly was in the White House)

who told him about the major elements in the Nixon Program…Then Schweitzer

was able to see Nixon’s speech on television (James, 220)

The disregard for

the institution meant to keep stability in the world economy is interesting

because it introduces the position of the US Government towards the IMF.

It has been used as a tool of US foreign policy but not kept in regard

for purposes of international financial stability. The 1970’s was a time

of cheap money and loan pushing as a result of the deregulation of the

currency and gold markets. With the end of fixed parity and the dollar/gold

standard, raw materials prices soared in US$ prices as exporters sought

to put some order into those markets upset by the major changes after

the Smithsonian Agreement of August 1971. The dollar price of gold went

from 35 dollars an ounce to 455 dollars an ounce by 1980 and commodity

prices tended to follow a gold reference which increased substantially

reflecting the devaluation of the US dollar. According to Hammes and Wills,

commodity prices in gold remained stable during the 1970’s.

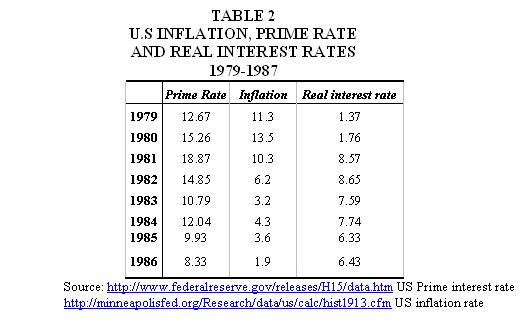

The effective real

interest rate of US dollars plummeted with the prime rate reaching an

average of ?0..75% between 1974 and 1975 while inflation reached an average

of 10% per annum. This opened the way to much irresponsible borrowing

and lending . The credit cycle entered its boom period at the time, to

put it in Marichal’s terms.(1989) Actually the credit cycle started in

the 1960’s and accelerated as the supply of credit curve became steeper

with more dollar liquidity entering the international banking circuits

after 1971..(Ugarteche, 1986) Inflation soared in the United States from

3.2% in 1972 to 11% in 1974.(table 1) The effects of the oil price increase

in December 1973 was to be seen starting from mid 1974 and more clearly

in 1975. US inflation in 1973 and 1974 resulted from excess dollar liquidity

rather than from oil price shocks. Those came later and were added to

the first.

|

At the time developing

nations borrowed because either: 1) they had oil and could afford it,

especially at negative or very low rates, 2) because they did not have

oil and had to cover massive deficit and could afford it at those rates.

Lenders, public and private, overexposed themselves, while debtor nations

held uncontrolled budget and balance of payments deficits around the world.

The exchange rate fluctuations of the dollar and the search for a more

stable exchange rate mechanisms on the side of the French, led to what

is known as the Rambouillet agreement. The meeting took place at the French

town on November, 15, 1975 and both sides reached and agreement as to

the need to have an orderly exchange rate mechanism without fixed parity.

There was the mistaken perception that U.S. dollar financial flows would

be cheap and permanent as the average interest rate between 1973 and 1977

was practically nil. At this time, after many discussion as where to go

with the IMF, some changes where introduced particularly referring to

Article IV. The IMF would be kept out of the daily follow-up of exchange

rates made by France and The United States. (James, 1989,: 269)

In lieu of a system of rules, the new article IV set about a new philosophy

of management of the international economy. Section 1 referred to the

obligation of members of the Fund “to assure orderly exchange arrangements

and to promote a stable system of exchange rates” (that is not “a system

of stable exchange rates”) Section 4, indefinitely postponed (at least

as long as the United States was opposed) the readoption of par values.

“The Fund may determine, by an eighty five percent majority of the total

voting power, that international economic conditions permit the introduction

of a widespread system of exchange arrangements based on stable but

adjustable par values”…In practice it seemed unlikely that a new stable

system would be put in place soon. (James, 272)

The conditions

after the Rambouillet meeting weakened the Fund to the point that economic

policy summits between leading nations replaced previous discussion at

the IMF. The G4, then G5 and later G7 countries made up a small “Library

Group” (James, 266) that held its own discussions that allowed them to

coordinate their economic policy. Giscard d’Estaing described it as “a

private, informal meeting of those who really matter in the world”, (James,

267) whilst the other lesser developed economies held their discussions

at the IMF and followed its prescriptions to a greater or lesser degree.

In the mid 1970’s

some debtor nations started entering payments problems, such as Zaire,

Jamaica, Egypt and Peru so in 1976 a new role was quickly found: that

of “policeman for the banks” and advisor to debtor countries for debt

negotiations. Exceptionally in 1976, President Ford obliged the British

Labour Government to swallow a two year IMF standby with all its conditions

in 1976.(James, 281) The Extended Fund Facility was introduced at the

Fund in 1975 with increased conditionality than the one relating to one

year standby loans. Then executive director stated that lending without

conditionality made no sense. This became the rule for longer period adjustments.

G7 creditors gathered at the Club of Paris do not consider renegotiating

a debt without the Fund’s approval. It was a policeman with a big stick

It must be pointed out that both the G7 and the Club of Paris are informal

associations of leading rich country interests..

In the late 1970’s

however real interests rate started to increase as stagflation began to

be felt and Volcker applied a restrictive monetary policy from 1979 onwards.

Eventually, in 1981, Reaganomics was introduced to reactivate the US economy,

injecting a massive budget deficit while keeping the brakes on monetary

supply. The consequence was a leap in real interest rates from 1.76% to

8.57% between 1980 and 1981 with the inverse effect on commodity prices.

As inflation was put under control, U.S. domestic interest rates starting

to go down and real rates were reduced. It took until 1992 to return to

more or less normal average rates from before the crisis although they

never returned to pre 1972 real rates.

US monetary policy and the debt problem

The pattern of real

interest rates over fifty years b has four well defined periods:

1. from 1956 to 1972 real interest rates had an

average of 2.67%.

2. From 1973 to 1978 it dropped to 0.53% with a period of negative

rates at the bottom between 1974 and 1975 of ?0.75%.

3. From 1979 to 1986 it leaped to 6.05%

4. From 1987 to 2005 it reduced to 4.46% |

All debtor nations

with a primary exports base, entered defaults from 1982 onwards almost

simultaneously when together with the rise in interest rates, commodities

prices collapsed, and net resource transfers became sharply negative.

From then on, in a continuous motion, debtors refinanced unpaid capital

and interest due of the past year making them repayable in the following

eight years. This increased the debt service ratio in a ladder effect

for the next nine years. The IMF seemed to worried about the stability

of the United States banking system more than about the stability of developing

economies and acted accordingly. It served for all practical purposes

as a foreign policy instrument of the US Treasury more than as a stabilizer

of the world economy. Says Boughton (21), “Major parts of the world, however,

suffered some of the most severe economic stresses of the century”. How

did this come about?

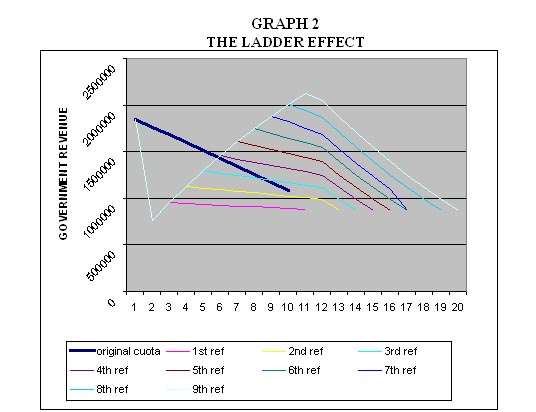

GRAPH 1

|

The ladder

effect

The ladder effect refers to the escalating weight of refinancing on Government

revenues if capital is rescheduled every year and interest remain paid,

given revenue restrictions. The existing bank refinancing mechanism of

the 1980’s led to the following effect: The first year of default, the

quota of unpaid capital would be restructured into a ten year loan. For

example, in a 10 million dollars, ten year loan, one million be the yearly

amortization quota. This amount would be restructured into a another ten

year loan. If revenues fell during the entire decade, using this mechanism,

the debt increased as follows. In the fourth round of refinancing, the

debtor would be induced into a total default because it reaches the breakeven

point between paying the entire original debt or rescheduling yearly payments,

considering interest was kept up to date. This rescheduling mechanism

sent the countries into default rather than help them recover payback

capacity. The procedure of refinancing the unpaid capital year by year

was what in the end made the debt unmanageable. Had the entire stock of

the debt been reprogrammed in the first place over a longer payback period,

this escalating weight would not have occurred.(see graph 2)

|

The thick line is the original payback schedule and the thinner lines

are the increasing steps in terms use of Government revenues starting

from rescheduling 1 through 9, where the first three refinancing reduced

the amount of the quotas, but starting from the fourth, it is above the

original payback schedule. There were nine rounds of refinancing during

the 1980’s. At then end the stock was still due, but the amount really

paid was almost twice what it would have been if payments had been made

on time in the first place, had there been revenue to do so.

The

schedules after nine rounds of refinancing extend over a 20 year period

overall, as each round has the same ten year payback period as the original

loan. The same exercise with total debt rescheduling over twenty years

produces a vastly different scenario.

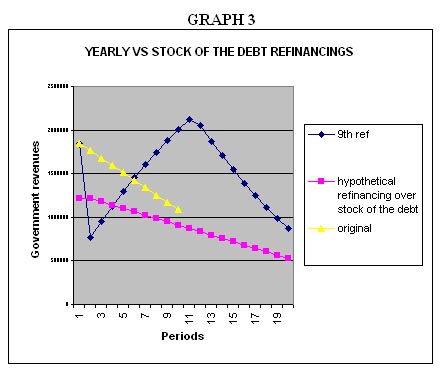

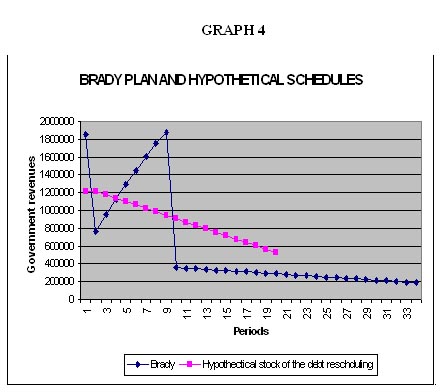

The

Brady Plan solution in fact reduced the stock of the debt by half after

debt service had more than covered the stock of the debt under the guise

of increased overall interest payment in each round. The 10 year ten million

dollar loan ends up being paid back over thirty four years and costing

20 million dollars. Over the initial 10 year period, with nine rounds

of refinancing, this 10 m dollars loan cost 13 millions and the stock

of the debt remains intact at 9 million dollars. If Brady had not come

with a plan to reduce the stock of the debt to market values, which reduced

them by around 55% and reduced interest rates to 4%, the debt would not

have been manageable. (see graph 4)

|

The

really existing rescheduling mechanism was set in place with IMF assistance

and coercion, with no appearance of the institution to side with the debtor

in the externally generated problem. If the object of the IMF was to maintain

international stability, the result is mixed, while it did prevent a possible

US banking crisis, on the other hand it launched Latin America and Africa

into a depression metaphorically referred to as “the lost decade” and

the ensuing policies have not been able to recover what was lost in incomes

and production after 25 years. The cost of the debt during the 1980’s

was more than what was borrowed and then the stock remained the same at

the end of the decade as a result of this ladder effect. Between 1982

and 1989 rescheduling were done yearly while flows remained negative and

both export revenues and tax incomes dropped sharply in Africa and Latin

America as commodity prices fell and economic activity was depressed.

|

The

role of the Fund during this period seems more related to the US Treasury

and U.S banking stability while they made sure there was a negative net

flow of capital in developing economies in order to maintain world stability.

They were more worried about adjustment policies and how to face the high

costs of the debt rather than doing something about the real origins of

the international monetary strains. Stiglitz refers to the Latin American

experience with the IMF as correct, as having done the right thing, however

the debt management experience was not only unfair, but unreasonable.

IMF policies did not tackle the problems of high international interest

rates and falling commodity prices but instead centered on the State as

an inefficient assigner of resources, following the new classical synthesis.

Inflation, on the other hand, did not go down during the 1980’s, but inversely

went up and this led many Governments to shy away from Fund prescriptions

because their effects where not positive and they became politically difficult

to swallow. Some Governments applied heterodox policies trying to get

inflation under control but in all three cases it proved positive in the

very short run but useless in the medium term as they all landed in hyperinflation:

these are Brazil, Argentina and Peru between 1985 and 1989. As the IMF

macroeconomic model became improved and the international interest rates

went down slowly, the external sector became more manageable. Nevertheless

the consequence of the compression of consumption and savings was negative

for both the economics and the politics of the region during the period.

What followed in terms of recovery of flows of capital, seems to have

been related to privatization and opening up of the financial sector,

mainly. It did not last more than six years and with international imbalances

adverse to developing economies, after 1998 the flows for Latin America,

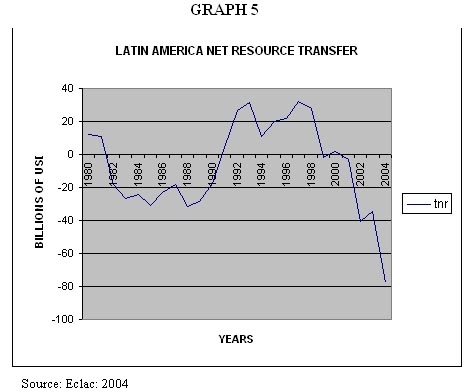

at least, turned negative again. Over the last twenty five years, there

have been six years of positive flows according tom ECLA. The region loses

capital permanently. Included in graph 5 are long term financial flows:

direct investment and long term loans.

|

The Brady Plan

Some

discussions were held within Latin America in order to face what was a

very serious economic problem that led to dire political consequences

in the region. The IMF kept to the side of these. The discussion on the

use of bonds in order to have a long run, one time reprogramming, was

made in Latin America by Ugarteche (1984) Luis Carlos Bresser of Brasil

in 1987 (1995), but also was a major part of the discussion held amongst

Latin American academics as to how to come out of an entangled system

that was depressing the region. In every major debtor country someone

was speaking of bond conversions using the XIXth century history of debt

crises solutions. In the US, Prof. Kenen from Princeton brought the point

up in the early 1980’s. There was a consensus in Latin America by the

time the Baker plan was designed in 1985, that only a long payback period

with a return to the original amount owed in 1981 would make the debt

payable. It was clear that the debt incurred between 1982 and 1985 was

not voluntary for any of the parties, neither creditors nor debtors. That

is why the Baker Plan failed in 1985. This led to the consensus amongst

debtors that very long term bonds were the only reasonable answer. The

Brady Plan in 1989, has elements of the Bresser Plan proposed in 1987.

Debt reductions under the Brady Plan however were nowhere near to the

debt increase caused during the decade by continuous refinancing and the

unusually high US$ interest rates.(see graph 3) The IMF, and Witteveen

at the time Ezxecutive Director, were more concerned with “correct” economic

policies, than with the external elements that had induced an economic

crisis of major dimensions to dozens of countries.(James, 322) Conditionality

was then the name of the game and the sole object of the Fund was that

countries follow their prescriptions in order to restore a sound economy.

The only one that was not induced in this direction, and the IMF has no

power to make it do so, is the United States.

Boughton

suggests that the changes required from the Fund were met at the various

breaking points between the 1970’s and 1980’s:

The Bretton Woods system of fixed but adjustable exchange rates came

under strain and collapsed, and a more flexible system was negotiated.

Because the new system imposed few constraints on national economic

policies, the Fund was drawn into a more active “surveillance” role

in overseeing its implementation. Moreover, as the landscape of the

world economy became more precarious, the Fund was drawn into a more

active lending role that required a deeper and more sustained involvement

in the formulation of macroeconomic policies in countries facing economic

crises. During the 11 years covered in this work, 1979 through 1989,

a confluence of upheavals propelled the 01institution into a more central

and pervasive role than ever before. (Boughton, 2001: 1-2)

Throughout

the 1980’s Governments were pressed by the IMF and the Club of Paris,

to pay up and follow their policies leading to high, and very high inflation

? after the adjustment programmes were introduced and tightened? which

over time generated adjustment and refinancing fatigue. Incomes fell,

growth fell, wages fell, consumption as a result also fell, political

instability grew, income distribution worsened. Only then inflation was

controlled and exports grew.

At

the same time the Soviet block collapsed and its member countries opened

to western trade, China grew into a major trading partner for most of

the west and the role of the State was reduced as market orientated policies

were put in place in every country either voluntarily or through adjustment

policies. IMF adjustments agreed upon at the Institute of International

Economics conference of 1982 were applied throughout the developing world

as debt problems surged as a result of the above mentioned interest rate

explosion. The uniformisation of policies allowed for what is now called

“globalization” and fostered the new trading blocks, including those frustrated

like the FTAA. It accelerated intra Asian trade and later in 1992 the

formation of the European Union with its 25 member country projection.

Africa was left for humanitarian aid and Latin America lost relevance

all together. Mercosur was formed in 1994 between Brazil, Argentina, Uruguay

and Paraguay and the Andean Community underwent a refurbishing from Andean

Pact to Andean Community of nations as a sign that it had modernized and

left the role of the State aside. N o doubt the IMF was a weapon of the

G7 but more so of the US Treasury in the fight towards globalization understood

as open markets for goods and services, particularly as the Soviet Union

collapsed.

The philosophical and economic barriers between North and South and

between East and West remained in place at the end of the 1980s, but

the means for destroying them were nearer and more evident than ever

before in history. This “silent revolution,” as Michel Camdessus named

it in a more specific context, brought an unprecedented importance to

the IMF as every region in the world struggled to keep its footing in

an increasingly dynamic and global economy….To a great extent, the silent

revolution of the 1980s resulted from a shift in economic philosophy

toward a new classical synthesis in which government has an indirect

role in, but not a direct responsibility for, ensuring national economic

prosperity; in which private economic activity is promoted through good

governance and the development of physical and social infrastructure.

(Boughton: 3)

The

IMF was at the time the guarantor of these “sound” economic policies and

any doubt as to this matter were eliminated by the Club of Paris who would

not sit down with the debtor nations unless the IMF had done its work.

Boughton, IMF historian, admits the Fund is a political organization and

that it played its role at the time. It must also be understood that the

universalisation of the new classical synthesis had a political interest,

over and above, its intellectual importance. Debtor governments had to

comply to conditionality based on the new classical synthesis in order

to return to the next round of debt negotiations at the Club of Paris

and the London Club, for example. Primary budget surplus became as much

a rule as trade liberalization, privatization and elimination of subsidies

and market distortions. That this was a prescription for some countries

and that in that measure it gave facilities to other stronger countries

is not mentioned by Boughton. That the flying geese concept of Asia as

having first started with import substitution, then advanced to substituting

complex imported products, then advanced to simple export substitution

and later ended in complex goods export substitution was ignored. Ministry

of Finance officials spent many years during the decade negotiating with

the IMF, the Club of Paris, the London Club and readjusting IMF projections,

in order to jump the hurdle of not being in arrears and only to start

the same exercise as soon as the previous cycle was completed. IN the

end, import substitution policies were eliminated, with no later stages

developed, and whatever the result, that was the optimal outcome of the

model. Evidently, the result of IMF/WB conditionality in terms of economic

growth is not very flattering, as can be seen below for Latin America

as a whole. It appears that the economy grew until 1980 and then it has

followed a seesaw pattern approximating 0 per capita growth average for

the 1990’s. While this happened, European country deficits were increasing

as were US deficits in the pursuit of contra cyclical policies. The major

surplus country was China followed by Japan. The leading deficit country

is and has been the United States.

|

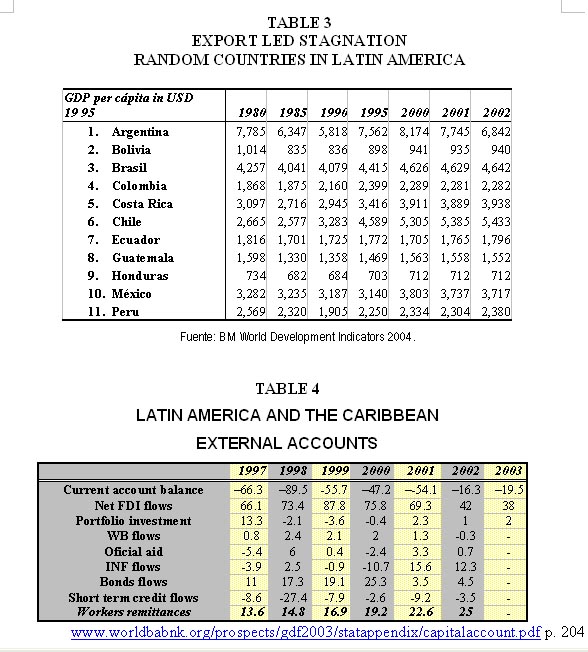

If

we take income per head of 1980 as the base year, before the so called

debt crisis erupted, and see the point at 2002, last data provided by

the World Bank in 1995 dollars, it is evident that out of eleven countries,

Chile stands out as having doubled its per capita income.(see table 3)

The rest are more or less in the same place, some are behind 1980 like

Bolivia, and Honduras, but one has advanced some: Costa Rica. Aggregate

growth has been reduced to nothing according to World Bank data on constant

95 dollars. For all the pain of the adjustments and the massive political

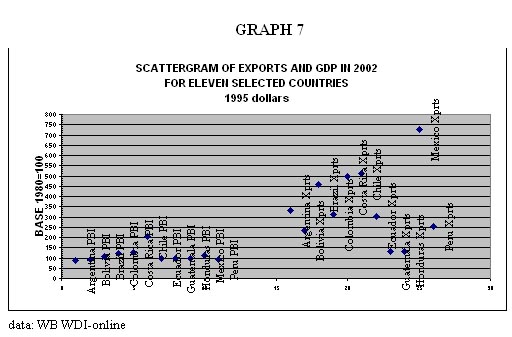

and social problems introduced, the results are meager. Exports have grown

substantially but bear little relationship with GDP per capita when we

take 1980 as the base year. (see graph 6)

|

Conditionality

seems to have supported export growth and inflation control but not income

growth, or even less, wage recovery or employment. There is not much to

be said about exports and growth. In terms of IMF mandate, this means

that they have facilitated the expansion of world trade but have failed

at maintaining high levels of employment and real income, have proved

incapable of keeping exchange stability in Mexico (1994), (the devaluation

went from 3 to the dollar to 10 to the dollar), Thailand (1997), Brasil

went from 1 real tom 3 reales to the dollar (1998) and Argentina, from

1 to 4 to the dollar (2001) are to witness, nor have they been able to

lessen the degree of disequilibrium in the international balance of payments

of member, as is witnessed by the US deficit and the major Chinese surplus.

The

result after twenty five years is that the balance of payments of Latin

America on the whole is financed by emigrants who cannot find proper employment

in their home country and growth is very unstable. Amongst the sources

of foreign exchange in the economy, after the net revenue of goods and

services comes the revenue from exports of people, just below foreign

direct investment, but over portfolio investment, tourism, and loans.

|

Co responsibility and the IMF

Creditor

debtor co responsibility was raised since the beginnings of the so called

“debt crisis”. The first time the point came up was at an Organization

of American States conference on external debt, meeting in Caracas, September

7, 1983 which concluded with a declaration under the name Bases para un

entendimiento where shared responsibility was brought forward in view

of high US interest rates, inflexible IMF conditions and a short leash

policy of debt renegotiation. At the Latin American Conference of Heads

of State held in Quito, January 9 to 13, 1984 the concept of co responsibility

was recognized as a major issue at the political level and where they

demanded that IFIs, international private banks and leading Governments

take their share of their co responsibility at the same time as Latin

American and Caribbean countries made their best efforts to keep their

payments to date. James Baker, U.S. Secretary of the Treasury made at

the IMF 1985 Seoul spring meeting a debt management proposal which was

a recognition of co responsibility. The Catholic Church made its first

report on debt and called for co responsibility through Un Informe

Etico de la Deuda Internacional made by the Pontifical Commission

in Rome in 1986 which then led to the Jubilee movement in 2000. The G7

made the same recognition in 1988 when it discussed the Toronto terms

of debt management. The meaning of co responsibility does not seem to

be clear. Eurodad demands that IFIs “need to publicly acknowledge the

roles they played in exacerbating indebtedness in poor countries”. This

is true not only for the poor countries but for all developing nations.

Co responsibility then as now was a ´political declaration that bore little

effect in terms of policies and “paying the price”. The debtors paid the

price mostly. The IMF did not claim any responsibility of the creditors

in the loan terms and interest rates as the case should have been given

its multilateral essence.

The

1980’s saw how Governments exported more than half of national savings

at the cost of adjustment policies which reduced Government wages, education

and health expenditures, thus disorganizing Government bureaucracies and

overall creating conditions leading to a loss of governance. Boughton,

the Fund’s historian refers to this as

The 1980s brought more economic success than the 1970s, especially

through the stabilization of prices. Although global output growth continued

the declining trend that began in the 1970s, a gradual improvement in

policymaking laid the groundwork for the noninflationary growth that many

countries would enjoy in the 1990s. Major parts of the world economy,

however, suffered some of the most severe economic stresses of the century.(21)

By the end of the 1980’s it was clear that inflation could be put under

control but that the impact of reforms on economic growth was adverse

to begin with. The hope was that this would open up the conditions for

future growth on a new basis. The sole example was and is Chile. The private

financial sector could not finance the world alone, and some conditions

were required in order for loans to be recovered. It was not clear then,

nor now, if those conditions are the ones set by the IMF, as was seen

with the Mexican crisis of 1994, the Asian crisis of 1997, the Russian

crisis of 1998, the Brazilian crisis of 1998, and the Argentine crisis

of 2001., to name but a few.

.

The argentine crisis and the IMF credibility gap

The

first problems of credibility began in Thailand and Stiglitz has written

about them extensively. The Stiglitz/Summers debate was a centrepiece

that aired how the IMF lost its reputation and how the US Treasury, in

spite of ignoring the IMF for itself, uses it for foreign policy purposes.

Summers made sure Stiglitz left the Word Bank, where he held the post

of Executive Vice President, and then “One of Stiglitz’s proteges, Ravi

Kanbur, had been put in charge of writing the Bank’s World Development

Report 2000 focusing on world poverty. The Report was to be released

in September but by June Kanbur felt in all conscience he couldn’t continue.

When the report finally appeared, Kanbur’s sections on the necessity of

social spending, redistributive tax policies and control of speculative

capital were either gone entirely or had been significantly watered down.

With the help of pressure from the US Treasury the politics within the

Bank remained firmly in favour of the Washington Consensus.” (New Internationalist

336,July 2001) Kanbur was also sacked.

The

essence of the discussion was the speed with which capital accounts were

opened and the usefulness for Wall St of Summers recommendations from

the Treasury versus a more discrete approach to capital movements. In

the end the Asian crisis, says Stiglitz, is a by product of market fundamentalism,

aggravated by IMF recommendations in the same direction.

Unfortunately

for the Fund, the following year after this debate (2000), the Argentina

crisis exploded. In brief, Argentina decided to follow a convertibility

plan in 1990 in order to brake inflation and stabilize the economy. This

fixed rate was at 1 peso 1 dollar par and worked fairly well between 1990

and 1997 but in 1998, when Brazil devalued its currency also from par

1 to 1, to 3 reales to 1 dollar, the strains appeared in Argentina’s a

accounts. Brazil was a main trading partner of Argentina at the time since

the signature of Mercosur, an integration scheme that includes Uruguay

and Paraguay. The impact of the Brazilian devaluation on the Argentine

economy was quick and strong, resource transfers started to be negative

as depositors took their money out and new foreign investments did not

materialize. The level of foreign debt had doubled during the 1990’s and

the national budget was strained to keep its debt payments to date. In

face of this, the decision made in Buenos Aires with IMF support was to

keep the exchange rate fixed at 1, and tighten monetary supply as much

as possible in order to prevent a devaluation. The result by 2001 was

that liquidity shortages forced barter, that alternative monies were introduced

in the different States of the Nation and that foreign debt increased

substantially in order to finance the rate of exchange. The private sector

could only borrow abroad so overall total indebtedness grew substantially

in the last two years before the crisis. By December 2001 this was no

longer manageable and the IMF decided to suspend its standby programme.

One week later they declared a default. Institutionally the IMF did not

learn the Mexican lesson from 1994: that floating rates are better than

fixed rates when there is a sudden serious imbalance as a result of an

external factor.

In

the aftermath, the research director of the IMF wrote a book titled Argentina

and the Fund : from triumph to tragedy (Mussa, 2002) where he describes

the problem and washes the IMF’s hands from what occurred. As Argentine

GDP was contracting in 2002, the IMF was making a public relations campaign

on how it was not responsible for what its advisees do. How they are only

external advisors and how it was a real shame that Argentina had lost

its opportunity. It did not rescue Argentina nor did it assume any responsibility

with the creditors as to what happened. Even less so with the people or

Argentina.

By

2004 Isabelle Mateos y Lago from the IMF wrote an independent evaluation

report paper where she did an outside evaluation and said:

The role played by the International Monetary Fund (IMF) deserves special

attention for at least three reasons. First, unlike the cases of Indonesia

and Korea, where the IMF had no program involvement for several years

preceding the crisis, in Argentina the IMF had been almost continuously

engaged through programs since 1991 (Box 1.1). Second, again unlike the

other cases, the crisis in Argentina did not explode suddenly. Signs of

possible problems were evident at least by 1999, which led the government

to seek a new Stand-By Arrangement (SBA) with the IMF in early 2000. Third,

IMF resources were provided in support of Argentina’s fixed exchange rate

regime, which had long been stated by the IMF as both essential to price

stability and fundamentally viable. Drawing lessons for the future, in

evaluating the past, and especially in determining accountability, it

must be kept in mind that much of what we know now may not have been known

to those who had to make the relevant decisions. (2004 a)

In the press conference where the report was presented, this was added

:

In terms of the assessment of the fundamental causes of the

crisis, it is our judgment that it was essentially a combination of the

failure of Argentinean policymakers throughout the 1990s-and during the

crisis period of 2000-2001-to take the necessary corrective action to

make sure that domestic policies were compatible with the choice of the

exchange rate regime. (2004b)

…

But the message is very clear from the Argentina case, too, that many

programs that are not dealing with the most fundamental structural problems

underlying vulnerability--and in this case it's fiscal structural problems--are

in the end not very productive. And so, you know, the Fund should perhaps

not have had so many programs with Argentina during the 1990s.

…

So our main message about the weaknesses of the Fund's role during this

period was essentially not with the initial decision in January 2001.

As I said, judged in a probabilistic sense, it could be justified. But

it was with the lack of sufficient contingency planning, and because of

that the decision to continue supporting a strategy that under most reasonable

judgments one could have concluded, even with information at the time,

was not working.

…

On the August package, we're absolutely clear in the report that we think

it was a mistake. And, in fact, we're also saying that the May disbursement,

you know, the Third Review under the program, was also a mistake in our

view because the situation was unsustainable, clearly unsustainable.

…

We're suggesting that these $9 billion essentially that were disbursed

between the spring and September could have possibly or hopefully been

put to more productive use if they had been used in support of, say, a

move to Plan B, a devaluation, or something like that, could have been

used to limit the overshooting of the currency depreciation, and in the

meantime would have avoided further deterioration in banks' balance sheets,

would have avoided another six months of a really sharp recession.

The IMF was not responsible in the last instance, says Mateo, because:

The IMF is only one of the actors involved. In practice, the country

itself is ultimately responsible for its policy decisions. This is especially

important when the underlying policy choices are strongly owned by the

country? as they were in Argentina.(8:2004a)

This

disclaimer weakend the credibility of the Fund more that it helped understand

the Argentine crisis. If the IMF was supporting a fixed exchange rate regime,

and financing it, it is not a mistake of argentine policy makers, but an

agreed a policy with the IMF. If there was no contingency plan if stability

was not maintained, then it was incompetence on both sides. Added to Mussa’s

book, the Mateo work finished burying the institution. In the mean time

the new Argentine president took it upon himself first to get the proper

economic advise in order to have economic recovery. The result can be seen

in the table below. Secondly, he negotiated the foreign debt, bloated in

the last IMF supported mega swap of 2001, and reduced the stock of the debt

by 75%, without IMF advise. More than 80% of the creditors accepted these

terms. Then he decided to pay the IMF back its loans so they would no longer

require their services.

The IMF moved in to the centre of a credibility gap. It showed the world

it was not a guarantor of sound economic policies as it was meant to be,

but equally it was not a loan guarantor nor was it a lender of last resort.

What is it then? The Asian Monetary Fund, The Asian monetary

unit and the future of the IMF

At the time of the Asian crisis, the Japanese Government launched the

idea of having an Asian Monetary Fund that would take care of Asia’s balance

of payments problems. When the Japanese Government announced its intention

to do so, the US Treasury expressed its opposition to the idea and reinforce

the role of the IMF. Bergsten (1998) suggests that it generated fears

that it could undermine the leadership role of the IMF and foster a split

between Asia and the United States. An Asian dominated fund would reduce

its influence in the region and would have shattering effects on the IMF

and the World Bank.(Lipscy, 2003).

Nevertheless, in Chiang Mai, Thailand, in May 2005, the ASEAN country

members led by Japan, China, South Korea and including the ten country

members, agreed to expand their bilateral swaps and form a certain protected

currency area. This initiative covers sixteen countries and has a 40 bn

dollars fund.. (http://www.aseansec.org/afp/115.htm)

On

the other hand, in Latin America, Venezuela has acted as a lender of last

resort, purchasing central bank positions without conditions, thus allowing

the Argentine Government, to name one, the policy space to do what it

feels is correct in terms of inflation control and economic growth. Others

that have benefited from Venezuelan largesse are Bolivia, Ecuador and

Colombia. President Chavez has said he wants to have a Latin American

IMF.

Additionally,

from 2002 onwards Argentina first and Nigeria later, negotiated their

debt without the IMF, and both private and public creditors allowed them

to do so. At that point the credibility gap was so large it was pointless

to call in the IMF as a guarantor of either sound economic policies or

lender of last resort. The major debtors returned the Fund the money borrowed

from them ahead of schedule in a way of getting rid of conditionality,

thus earning degrees of freedom at a time of international uncertainty

on the future of the US dollar. In 1998, twenty one countries had standby

loans. In 2006, there are only four and Indonesia has announced it will

also pay the Fund ahead of schedule. The stock outstanding of debt owed

to the Fund was 138 billion US$ in 1998 and has been reduced to 35 bn

dollars in 2006. Bankers gathered around the Institute of International

Finance addressed the IMF chair stating that they had doubts on the effectiveness

of their recommendations”.(IIF, 2006) In brief, neither debtor Governments,

leading G7 governments nor bankers believe in the IMF any more.

In this context the Executive Director of the IMF has pursued a policy

of revival seeking a new role, much like in the past. Nevertheless it

is generally recognised that the representation system is not adequate

for the new world, that there is little transparency on elections, that

policies are not adequate and that they no longer serve as international

guardians.(Truman, 2005) Nothing will help get it back to where it was.

The IMF and the United States

The

issue of the US deficits and what to do about them is key to recovering

its credibility. It is evident that the US Treasury ignores the IMF recommendations

and that it prefers to blame the rest of the world for its ills than assume

responsibility for its misdoings.

Undersecretary

Adams of the US Treasury made a statement April, 19, 2006, where he describes

the US economic position:

We will also seek to advance fundamental reform of IMF governance.

Modernization at the IMF needs to reflect rapid growth in many emerging

markets and other key changes, such as the euro's advent. The IMF is

a shareholder institution; members' roles should reflect their relative

global economic weight. There is growing consensus on a two-step process.

The first step would involve a small ad hoc increase for the most underweight

emerging market countries around the time of the Singapore Annual Meetings.

But this must be credibly linked to near-term completion of broad second

step reforms. Such reforms should include revamping of IMF's quota formulas

to make GDP the key variable, or developing an alternative metric to

this end; achieving a further increase in emerging market countries'

weights; and examining concrete actions to rationalize Executive Board

representation. Fundamental reform also needs to bear in mind the voice

of poor countries. We are confident that all countries ? with a collective

interest in an IMF that is strong, legitimate, and relevant ? will help

to provide leadership and find a consensus. (Statement by Under Secretary

for International Affairs Timothy D. Adams in Advance of Meetings of

the G-7, IMF, and World Bank)

The IMF article IV consultation to the United States produced at the

same time says the following: http://www.imf.org/external/np/ms/2006/053106.htm

Reducing External Imbalances

7. The ease with which the United States has financed its

record current account deficit has been remarkable, but is unlikely to

be sustained indefinitely. A number of (possibly temporary)

factors, such as short-term interest rate differentials and increasing

demand for long-term bonds, have helped support the U.S. current account

deficit and dollar over the past year. However, most forecasters project

that the current account deficit will rise further in coming years, which

may begin to strain the global appetite for U.S. assets. Delaying the

inevitable multilateral adjustment will mean continued increases in U.S.

external indebtedness, magnifying the potential for disruption to exchange

rates, financial markets, and growth, both domestically and abroad.

8. Firm and vigorous implementation of the cooperative strategy

laid out by the IMFC last April would support an orderly resolution to

global imbalances, and the Fund will use its new remit for multilateral

consultations toward this goal. The United States has a

major role to play in addressing this shared responsibility, and its main

task remains to boost national saving, including by more ambitious fiscal

consolidation.

9. Leadership by the United States remains key to global trade

liberalization. With progress slowing in the Doha Round

negotiations, continuing U.S. commitment and initiative are essential

to generate new momentum for a timely and ambitious conclusion. It also

remains imperative to resist protectionist responses to global imbalances,

particularly as restrictions on trade risk creating significant harm to

the global economy. As we have long cautioned, the growing number of bilateral

trade initiatives by the United States and others could undermine the

multilateral trade system, and there would be merit in seeking agreement

on common disciplines.

Putting Fiscal Policy on a Sustainable Path

10. As highlighted in the Budget, demographic and other pressures

threaten both fiscal sustainability and the nation's future prosperity.

Spending on Social Security, Medicare, and Medicaid currently account

for over two-fifths of federal spending and is rising at an unsustainable

rate. While there is no doubt that entitlement reform is essential for

achieving a sustainable fiscal position, recent CBO analysis illustrates

that even significant entitlement reforms and cuts in other spending may

not be sufficient to accommodate the increased demands from an aging population,

particularly on public health systems.

11. With the Administration indicating that it will achieve

its objective of halving the deficit earlier than anticipated, the time

is opportune to establish a more ambitious medium-term fiscal anchor.

There will soon be the need to define a new objective consistent with

the Administration's longstanding commitment to deficit reduction. With

revenues continuing to be buoyant, we would again propose a target of

balancing the budget excluding the Social Security surplus over the next

five years. Such an objective would place the U.S. federal debt-to-GDP

ratio on a clear downward path and reduce the burden on future generations,

while providing the room needed to develop and phase in reforms of health

and retirement systems. This would require consolidation at a rate of

around ? percentage point of GDP a year, which would ease the burden on

the Fed for keeping economy close to capacity while raising national saving

and reducing global imbalances.

12. We agree that expenditure discipline should remain central

to deficit reduction, but revenue measures cannot be ruled out.

To be sure, there has been some success in slowing the growth of outlays,

but the Budget projects that the federal deficit will remain around 2?

percent in FY 2007, roughly unchanged in three years despite the strong

economic expansion. This suggests some risk that the deficit reduction

that is projected in subsequent years may be difficult to attain, especially

since it does not take account of ongoing operations in Iraq and other

fiscal pressures on revenues and outlays. Thus, action on both sides of

the ledger may be required:

- On the expenditure side, entitlements and defense commitments limit

the room for cuts, and the Budget already assumes that the ratio of

discretionary spending to GDP will be reduced to unprecedented lows

over the next five years. Indeed, recent Congressional debate over emergency

appropriations underscores how difficult it will be to contain discretionary

spending. Although budget rules cannot substitute for an underlying

commitment to fiscal discipline, this suggests that there would be merit

in re-introducing caps on discretionary outlays and pay-as-you-go (PAYGO)

requirements, which had been successful during the fiscal consolidation

in the 1990s. However, it would also seem prudent to extend the PAYGO

rules to include the impact of tax measures, as was the case under the

1990 Budget Enforcement Act.

- On the revenue side, the significant reductions in marginal tax

rates in recent years have supported economic efficiency. Although

it may be difficult to sustain these tax cuts while meeting the fiscal

burden from population aging, the priority should be on reforms to broaden

the revenue base. The President's Advisory Panel offered useful suggestions

along these lines, but consideration could also be given to consumption-based

indirect taxes?such as a national sales tax, a VAT, or energy taxation?that

would maintain revenue buoyancy as workers retire.

This gentle appreciation for what is a 6% of GDP deficit in a country that

reduces tax revenues by introducing tax cuts at a time when its fiscal deficit

is growing, does not follow suit in tone or in essence to the treatment

given member countries. Stiglitz said in the Wall St Journal of June 21,

2006 that the credibility of the Fund lies in what it is able to do with

the US. From the article IV report, it appears that not much. The IMF remains

a U.S. foreign policy tool ignored domestically by the US Government. The

Fund does not have the clout to make it enter into its net..

IMF

reform or international financial architecture reform?

After

the Mexican, Asian, Russian, Brazilian and Argentine crisis, is the Fund

required? Can it be reformed? Can it recover its credibility? There are

two ways of looking at this. Reform for what, should be the question. If

the element that launched the idea of reform is the fact that they can no

longer pay their way with such few loans and interest revenues, the issue

is domestic to the IMF. If the question is how to recover international

credibility, the issue is how to recover a multilateral actor. Credibility

has been lost by not having a transparent voting mechanism to elect the

Executive Directors and by keeping the 1946 gentleman’s agreement that the

World Bank chair went to the United States while the IMF went to the Europeans.

This is nowhere written but has been the de facto manner in which IFIs have

worked. It was designed as a rich man’s club in 1944 when the US was the

almost sole creditors in the world and the rest borrowed from it. As a result,

its veto power made sense. It was their money mostly. However by 2006, the

US is a leading world debtor, it does not have money but major debts, mostly

to Asia but also to Latin America and to any surplus economy that holds

reserves in US dollars instruments: namely Treasury Bills. Nevertheless

it holds its veto power which it uses as a foreign policy tool to prevent

loans to its declared “enemy” countries such as Nicaragua in the 1980’s

or Cuba, to name but two. This is an exercise of power with no real financial

substance given the US is now the world’s major debtor and that it owes

its money to Asian and Latin American countries, all with the exception

of Japan, lesser developed than itself. The IMF keeps from yesteryear the

size of GDP to measure the voting rights and the US is still a very large

economy, but the size of GDP does not reflect the financial capability of

the country anymore. Credibility has also been lost because they have not

been able to stand the pressures from crisis generated by their own model

of capital account opening in Asia or by their own advise on how to handle

exchange rates in various parts of the world.(see the more recent independent

evaluation on this matter, IMF 2006)

Paradoxically,

the US Under Secretary of the Treasury has said the IMF should do its original

mandate: “international financial stability and balance of payments adjustment”.

The problem says Truman (2005) from the IIE, is that the IMF can become

a development institution working solely with low income countries and lose

its relevance. For the IMF to recover its credibility and do what the US

undersecretary suggest it needs to do again, the institution would need

to have the clout to bog down the US deficits in the same way as they have

done with everybody else, including Britain in 1977-78..The Fund has become

weak and ineffective. Can it bail out the US in the event of a run against

the dollar? No. In fact, it cannot bail out any major emerging market in

the event of an exchange run, as was seen in Argentina, 2001, Asia in 1997

an Mexico,1995. All of these were stopped with the direct intervention of

National Treasuries that financed a substantial part of the rescue.. Truman

(14) suggests the Fund should reaffirm its central role in international

crisis, including large scale lending activities. He makes the point that

in the 1970’s no one spoke of the moral hazard element and that given financial

globalization there is more need today for a lender of last resort than

ever. This is a reflection on the path economic theory took between the

1960’s and today. Is the issue of moral hazard relevant in international

bank lending and financial rescues? Or is it confusing the issues of a closed

economy and private borrowing with those of public borrowing and an open

economy? Says Truman that capital accounts and the financial sector are

central to the IMF’s role in the XXIst century.

Seen

with more distance and less sympathy, Bello and de los Reyes (2005) suggests

reducing the IMF rather than either reforming it on its past basis or getting

rid of it. Without the resources it had in 1945 in terms of GDP, or more,

of the member countries it does not have the means to face future crisis.

Bello and de los Reyes suggests that the IMF’s Stalingrad was in Asia. “The

IMF was widely discredited, being seen as the architect of capital account

liberalization that created the crisis, and of the severe contraction that

followed.”(2005:1) Perhaps on top of its Stalingrad it had a Waterloo, so

Argentina really added insult to injury. Bello and de los Reyes stress that

“In Malaysia, Prime Minister Mohamad Mahathir defied the IMF by imposing

capital controls, a move that raised a howl from speculative investors but

one that ultimately won the grudging admission of the IMF itself as having

stabilized an economy in serious crisis. Many eminent establishment critics

agreed that the Fund “should have tried unorthodox combinations such as

fiscal expansion, monetary contraction, and capital controls.” (2005:1-2)

The

result of the crisis, is that with 45% voting power concentrated in the

G7 countries, and 17% in the US, when only 15% of the votes are required

for a veto, the institution does not reflect the new world economic actors.

Thus, they say, the IMF reflects more the interest of the G7 countries

than those of the rest of the World. This one way in which it is an arm

of US foreign policy. Bello and de los Reyes suggest that “For political

reasons, it may prove difficult to abolish the IMF. But it can be disempowered

and converted into a research agency tasked with monitoring capital flows.”(6).

They also suggest that “In the global financial architecture, regional

arrangements such as a regional financial institution can supplant the

IMF as a regulator of global finance.” (7) because crisis are regional

in nature and they can be stopped within a region.

Bello

and de los Reyes conclude by saying that “More space, more flexibility,

and more compromise--these should be the goals of the Southern agenda.

Robin Broad,(2005) looks into the World Bank and finds it equally inadequate

with more professionals doing academic work than reflecting on development

issues as they come up. She suggests that the World Bank failures can

be met with a sharp reduction in personnel and making them accountable.

The point is to shrink the institution rather than getting rid of it.

On the other hand, the Joint Economics Committee in the US congress ,

led by representative Saxton said “"The World Bank must be made more

effective and focused on achieving real results in reducing poverty and

misery in developing countries. The performance of World Bank projects

must be closely scrutinized to ensure that resources that should be used

to benefit the poor are not wasted. Further progress toward grant financing

of World Bank projects is needed. In addition, the World Bank could provide

technical advice, and foster needed institutional reforms," (JEC,

2006) Saxton concluded. The lack of results point in Braod’s direction

rather than inm Saxton’s. It does not function.

Mainstream

academics and opinion makers conform a crowd of abolitionists together

with critics from the other shore who want to get rid of the IMF and the

WB altogether. These include Akyuz, (2005) Walters (1994); Schultz, Simon

and Wriston (1998); Schwartz (1998) and Milton Friedman (2004) who argue

for closing down both the World Bank and the IMF on grounds that they

have done more harm than good, and have the capacity for continuing to

do more harm than good. Lissakers suggests that it needs to have bigger

facilities without conditionality in order to prevent major crises. If

it is true that it does more harm than good, this refers to the conditions

attached to the use of lifesavers and not to the fact that there is a

lifesaver. A bigger IMF without conditions for the first or second tranche

could have been an alternative but the possibility that with their capacity

to impose conditions they will do so again is high, and their nature of

doing so is itself a reason to think of having decentralized stabilization

funds. The regionalisation of monetary stabilization funds is a good idea

so long as conditions are not attached that muddle up its workings

In conclusion: towards a new international financial architecture

The

conclusion from the arguments of the role of the IMF and the Development

banks is that in the first place, the results of what has been done over

two and a half decades is not promising. If it is true that inflation

is under control and that budgets are better managed, on the other hand

the lack of results in terms of employments, wages and GDP per capita

point in the direction that the policies are flawed. It is evident that

exports grew but it also is evident that migration is the main source

of revenues and growing more quickly than the balance in current account

of the balance of payments. There is not much evidence of a relationship

between exports and growth in Latin America over twenty five years with

the exception of Chile. The speed of export growth does not imply a fast

economic recovery,.

Finally,

if Structural Adjustment Loan policies have resulted in this combination

of outcomes, the question is what is the role of a development bank? Should

the World Bank be placing conditions on loans in order to obtain structural

changes so that these results can be shown? Given it deals with development,

should it not worry about employment, wages, income distribution, and

basic health and education indicators as well as environmental degradation

and gender balance?

The

impression it gives overlooking two and a half decades of bad country

performance in Latin America is that they worry about the rich getting

on and that the poor should pay the brunt of the effort. Increased indirect

taxation as well as tax reductions for new investments have been at the

center of policy recommendations that have not produced growth, but have

generated more income inequality, Labour flexibility, meant to generate

more employment, has landed being a source of social instability, violence

and migration, instead. Opening of capital accounts has not been reflected

in increased investment rates. Export promotion has resulted in export

led stagnation. What is the purpose of the World Bank?

The proposed new architecture:

A

new international financial architecture is required and it must include

a new set of rules and institutions:

- A universal legal code that will make sure all creditors have the

same rights and all debtors the same duties, with the same enforcement

mechanisms. This is analogous to what has occurred with international

trade law in a process led by a UN commission called United Nations

Commission on International Trade Law. (UNCITRAL) Currently international

loans are signed using domestic laws of the US and UK.

- It is clear that these problems recur, an International Board of Arbitration

for Sovereign Debt is required as a new forum for negotiations instead

of the Club of Paris and London Club. It should have a small secretariat

as a part of the UN system as an international body that will function

regularly and used by UN member countries. UNCTAD would appear to be

the likely place since they have DMFAS and experience with dealing n

foreign debt.

- The IBASD Secretariat will recommend arbiters that will be selected

by creditors and debtors in even proportions with the presidency decided

by both sides in order to have an uneven number of board members. The

inspiration of the IBASD lies in what was proposed for the German debt

agreement of 1952. (Hersel, 1998)

- Collective Action clauses must be incorporated into all new instruments

in order for the recommendations that follow to operate. These consists

of clauses whereby a majority of bondholders represent all, using the

Mexican precedent.

- No creditor/debtor discrimination must remain and the elimination

of free riders is urgent in negotiations. Debt cancellation for the

poorest countries in this approach should be immediate and unconditional

given they have no payback capacity and that conditions placed on them

have further damaged their capacity to have economic development, even

less to work their way towards the MDG. The HIPC initiative n its three

phases has proven a failure. Negative resource transfers from countries

with income levels of under 1,000 dollars per capita with a PPP of about

the same or less, a substantial percentage of the population with AIDS,

and with massive undernourishment does not seem to speak of serious

bargaining but on the exertion of power by multilateral banks.

- If there was any evidence that HIPC conditions lead to better income

levels, they might be considered, but there is nothing of the sort.

HIPC conditions seem to confuse the issue that if Governments spend

more on social sectors, they are advancing, much the same as is that

more exports per se lead to more GDP growth, which they do not.. HIPC

would have been taken seriously into account if income per capita in

terms of constant PPP was improving or had done so. Nicaragua. Honduras

and Bolivia are cases in point. It is not only too little too late,

but inadequate.

- It is correct that up to 100% of multilateral debt can be cancelled,

but the concept should be to keep all creditor categories under the

same treatment until the negative net resource transfer becomes cero

or positive, and the conditionality should be related to economic, social

and cultural rights. The MDGs is one step in that direction.

- Regional stabilization funds should act as buffers against speculation

in the money markets and should also watch the trends of the capital

accounts of its member countries in order to suggest preemptive adjustments

if the case may be, lending ahead of time.

- The concept that the statistical office of the World Bank remain in

operations while the rest of the bank disappear is attractive as the

data gathering experience is high, and the capacity to distribute the

data and disseminate the data banks is broad.

- In the future, the new institutions should be kept from the influence

of foreign policy in such a way that they may work effectively with

all member countries and not be subject to the whims of any major partner.

BIBLIOGRAPHY

Akyuz, Yilmaz

“Reforming The IMF: Back To The Drawing Board”, Third World

Network. Geneva, November, 2005

Bello, Walden & Julie de los Reyes

“Can the IMF be reformed?”, International Regulations, Paris-Tokyo,

August, 2005, http://www.socioeco.org/forums/d_read/intreg/IMF_delosreyes_bello.pdf

Bergsten, C. Fred

“Reviving the Asian monetary Fund”, Policy bried 98-8, Institute

of International Economics, December, 1998.

Bresser-Pereira, Luiz Carlos

“A Turning Point in the Debt Crisis: Brazil, the US Treasury,

and the World Bank” en Revista de Economia Politica, 19(2) abril

1999: 103-120. Originalmente publicado em Sao Paulo: Fundacao Getulio

Vargas, Departamento de Economia, Texto para Discussao n° .48, novembro

1995.

Broad, Robin

“The World Bank” at Intreg, Tokyo-Paris, 2005,

http://www.socioeco.org/forums/d_read/intreg/

Borchard, Edwin.

State Insolvency and Foreign Bondholders. Vol. I. General

Principles. Yale University Press, New haven, 1951.

Boughton, James

-------- “Why White, Not Keynes? Inventing the Post war International

Monetary System” IMF Working Paper, WP/02/52,

--------Silent Revolution: The International Monetary Fund, 1979-89.

IMF Oxford University Press Washington D.C. 2001

--------“The Case Against Harry Dexter White: Still Not Proven”

IMF Working Paper No. 00/149, August 1, 2000

--------“The IMF and the Force of History: Ten Events and Ten Ideas that

Have Shaped the Institution”, IMF Working Paper No. 04/75, May 1, 2004

Corporation of Foreign Bondholders

First Report of the Council, London, 17th February 1874.

Thirty-first Annual Report of the Council, London, February 1904

Fifty-seventh Annual Report of the Council, London, 1930

Eighty second annual Report of the Council, London, 1955

Friedman, Milton.

“60 at 60: Is There a Need to Change the Structure of the IMF and World

Bank?” Emerging Markets 60th Anniversary Special,.2004

IMF

“The IMF's Advice on Exchange Rate Policy” - Issues Paper for

an Evaluation by the Independent Evaluation Office (IEO), June 23, 2006

Lipscy, Philip

“Japan’s Asian monetary Fund Proposal”, Stanford Journal of

East Asian Affairs, Vol. 3, No. 1, Spring, 2003 pp. 93-104

Mateo, Isabelle

“Report on the Evaluation of the Role of the IMF in Argentina”,

1991?2001, IEO, IMF, (2004a) in http://www.imf.org/External/NP/ieo/2004/arg/eng/index.htm

Transcript of IEO press briefing on Evaluation

Report on the Role of the IMF in Argentina, 1991-2001 , IMF Independent

Evaluation Office, Thursday, July 29, 2004 Washington, D.C. (2004b)

in http://www.imf.org/External/NP/ieo/2004/tr/eng/tr072904.htm

Mussa, Michael,

Argentina and the Fund : from triumph to tragedy .

Institute of International Economics, Washington D.C. 2002

Schultz, George P, William E. Simon, and Walter B. Wriston.

“Who Needs the IMF?” Wall Street Journal, 3 February,

1998

Schwartz, Anna J.

“Time to Terminate the ESF and the IMF.” Cato Foreign Policy

Briefing, 1998

Stiglitz, Joseph

“ What I Learned at the World Economic Crisis. The Insider

“ The New Republic 17apr, 2000

Ugarteche, Oscar.

-----El Estado Deudor - Economia politica de la deuda:

Peru y Bolivia 1968-1984, Instituto de Estudios Peruanos, Lima, 1986

Walters, Alan. (1994). Do We Need the IMF and the World Bank? London:

Institute of Economic Affairs.

Williamson, John

-----(2003) “The Washington Consensus and Beyond”. An article commissioned

by the Economic and Political Weekly.

-----(2004) “The Washington Consensus as Policy Prescription for Development”

lecture at the World Bank,

http://www.iie.com/publications/papers/williamson0204.pdf

Viner, Jacob

“Dos Planes para la Estabilizacion Monetaria Internacional”

El Trimestre Economico, Vol. X, no. 3, Mexico DF, 1943, pp.450-482

|